The Inner Loop Buyer's Honest Guide to Houston Flood Zones

The questions every buyer must ask before making an offer

Published: April 28, 2026 | By Raquel Refuerzo

Quick Takeaways:

- Houston flood zones are not what they were even five years ago. FEMA released new draft maps for Harris County in February 2026, the first comprehensive update in nearly 20 years.

- Being in Zone X does not mean you are safe from flooding. Harvey proved that across hundreds of inner loop neighborhoods.

- Flood insurance costs vary dramatically by property, not just by zone. Two homes on the same block can carry very different premiums.

- Texas law requires sellers to disclose flood history and flood zone location. Know what to look for on that form.

- Before you make an offer on any inner loop property, you should be asking five specific questions. This post covers all of them.

What Are Houston Flood Zones, and Why Do They Matter More Than Ever in 2026?

Here's the thing about Houston flood zones: most buyers think of them as a simple yes-or-no question. Is the house in a flood zone or not? The reality is far more layered than that, especially right now.

In February 2026, FEMA quietly released new draft flood maps for Harris County, the first comprehensive update since 2007. These new maps use updated rainfall data, high-precision terrain scanning, and better computer modeling than anything Harris County has worked with before. According to analysis of the draft, the 100-year floodplain could grow by roughly 130 square miles countywide, a 43 percent increase. Many areas previously designated as 500-year floodplain would shift into the higher-risk 100-year category.

What does that mean for inner loop buyers? It means a property that appears low-risk today could be reclassified within the next two to three years. These draft maps carry no regulatory weight yet, but the process has officially started. Final adoption is estimated around 2028 to 2029.

What Are the Different Flood Zone Designations?

FEMA uses a letter system to classify flood risk. The key ones to know are:

Zone AE and Zone A are the ones buyers usually worry about. These represent the 100-year floodplain, meaning a 1 percent annual chance of flooding. Over a 30-year mortgage, that translates to a 26 percent chance of experiencing a significant flood event. Lenders with federally backed mortgages will require flood insurance in these zones.

Zone X (Shaded) is the 500-year floodplain. Moderate risk. Flood insurance is not required by lenders here, but after Harvey, a lot of Houston homeowners in this zone learned the hard way that optional does not mean unnecessary.

Zone X (Unshaded) carries the lowest designated risk. Flood insurance is not required and is relatively affordable if purchased voluntarily. But as Harvey showed, minimal risk is not zero risk.

How the New 2026 Draft Maps Change Things for Buyers

The old maps were built on rainfall data from before Tropical Storm Allison in 2001. The new ones account for post-Harvey conditions and reflect current best available science. Some inner loop areas near Buffalo Bayou and other bayou corridors will see meaningful boundary shifts. Buyers purchasing today are buying into a regulatory environment that is in active transition.

The smart move: check both the current official map and the new draft map before making an offer. You can search by address at the Harris County Flood Control District's interactive map.

What Questions Should You Ask Before Making an Offer in the Inner Loop?

This is where most buyers miss the mark. They check the FEMA map, see Zone X, and stop there. Here is what you actually need to ask.

Question 1: Has This Property Ever Flooded?

This is the most important question in any Houston real estate transaction, and Texas law gives you real protection here. Under Texas Property Code Section 5.008, sellers are required to disclose previous flooding from natural events, previous water penetration into the structure, whether the property is wholly or partly in a 100-year floodplain, and whether it is in a 500-year floodplain or a floodway. The Seller's Disclosure Notice is your first line of information.

Read every answer carefully. Vague or blank sections are a red flag. Texas courts have ruled that sellers who leave disclosure items incomplete face real legal exposure, and your buyer's agent should be flagging any incomplete sections immediately.

A property can be listed as "did not flood" during Harvey and still have a history of street flooding, water intrusion, or drainage issues. Ask specifically about all events, not just major storms.

Question 2: Is There an Elevation Certificate?

An Elevation Certificate is an official document prepared by a licensed surveyor that measures the property's elevation relative to the Base Flood Elevation (BFE) set by FEMA. If the seller has one, get it. If they do not, you can commission one as part of your due diligence for a few hundred dollars.

Why does it matter? Because under FEMA's Risk Rating 2.0 system, two homes in the exact same flood zone can carry dramatically different insurance premiums depending on their individual elevation, distance to water, foundation type, and other factors. A home that sits three feet above the BFE is in a very different position than one sitting at or below it, even if both appear as Zone AE on the map.

Question 3: What Will Flood Insurance Actually Cost?

Do not assume. Get a real quote during your option period. In 2026, median NFIP flood insurance premiums in Houston are around $1,574 annually, but Zone AE properties range from just over $1,000 to more than $4,300 depending on the specific property. Zone X properties in Houston show a median premium of around $593, though some pay significantly more. Private insurance is cheaper than NFIP in roughly 84 percent of Houston cases, so always compare both.

Also check whether the seller's current premium is grandfathered at a subsidized rate. If it is, that rate may not transfer to you. Ask the seller's insurance agent directly.

Question 4: What Has Been Done to Mitigate Flood Risk?

Inner loop Houston has seen substantial investment in flood mitigation since Harvey. The 2018 Harris County Flood Bond program funded hundreds of projects. Some areas that used to flood regularly now sit downstream of meaningful channel and detention improvements. Ask whether any mitigation projects have been completed near the property, and whether those improvements are reflected in the current maps or the pending draft.

Conversely, also ask about nearby development. New construction and impervious cover upstream can increase runoff to a neighborhood. This is especially relevant in fast-growing inner loop corridors like EaDo and Spring Branch.

Question 5: Can You Appeal or Remove a Flood Zone Designation?

If a property's lot is above the BFE but sits inside a mapped flood zone, it may qualify for a Letter of Map Amendment (LOMA). A successful LOMA removes the flood insurance requirement and can save thousands per year. The process requires an elevation certificate and a FEMA application, but there is no fee to apply. Many buyers do not know this option exists.

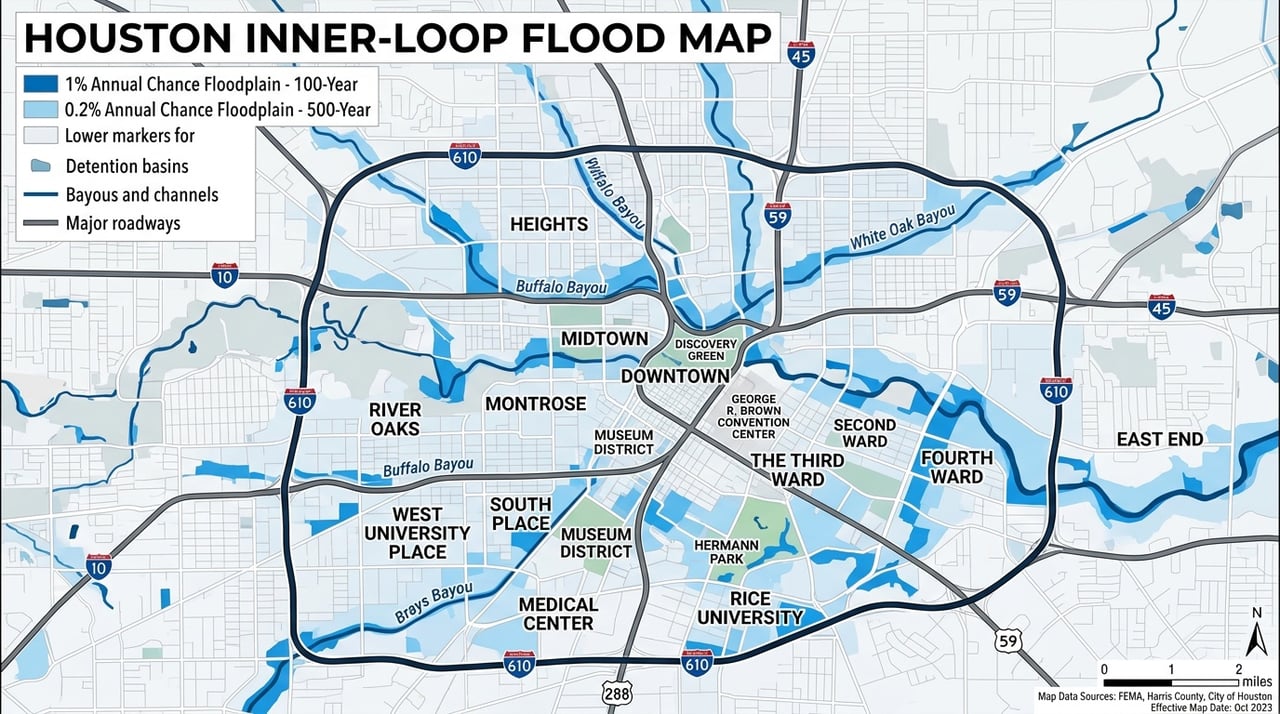

How Do Inner Loop Neighborhoods Compare on Flood Risk?

Not all inner loop neighborhoods carry the same level of risk, and within any single neighborhood, flood exposure varies block by block.

Neighborhoods That Performed Well in Harvey

Montrose generally held up well during Harvey. The northern edges along Buffalo Bayou had issues, but central Montrose, including the Hyde Park area, came through largely without flood damage. The Heights also performed well, though it is important to distinguish between Houston Heights proper and the broader Greater Heights area.

EaDo had no known residential flooding during Harvey, though the area does experience street flooding during heavy rains. Rice Military and the Museum District both came through relatively intact.

Areas With Greater Exposure

Neighborhoods along Brays Bayou, including parts of the Medical Center area, Braeswood, and Meyerland to the south of the inner loop, carry more meaningful flood exposure. The new 2026 draft maps specifically flag the Brays Bayou corridor for potential reclassification.

Midtown is generally considered lower risk, but proximity to Buffalo Bayou on the north side introduces variability. Property-level research matters here more than neighborhood-level generalizations.

The Data Table Every Inner Loop Buyer Should Study

| Flood Zone | Annual Chance of Flooding | Lender Insurance Required? | Estimated Annual NFIP Premium (Houston) |

|---|---|---|---|

| Zone AE (100-year) | 1% (26% over 30-yr mortgage) | Yes, if federally backed loan | $1,000 to $4,300+ |

| Zone X Shaded (500-year) | 0.2% | No | Optional, ~$400-$1,200 |

| Zone X Unshaded | Minimal | No | Optional, often under $600 |

| Zone AE with LOMA | May be removed | Potentially no | Reduced if LOMA granted |

Source: NFIP Risk Rating 2.0 data, Flood Insurance Guru Houston 2026 dataset

What Does the 2026 FEMA Draft Map Actually Mean for Inner Loop Buyers Right Now?

Nothing changes immediately, and that is important to understand. These are draft maps, not regulatory maps. Emily Woodell, spokesperson for the Harris County Flood Control District, has been clear: "Nothing changes right now related to flood insurance requirements or development regulations." The timeline from draft to full enforcement is estimated at two to three more years.

But here is why smart buyers are paying attention now: properties that are currently Zone X and likely to move to Zone AE will not require flood insurance until the maps are finalized and adopted. That means buyers purchasing those properties today may be getting in before a cost change that could add $1,000 to $2,000 or more per year. Some buyers see that as an opportunity. Others see it as a risk. Either way, you should know which category your target property falls into.

To check the draft maps, use FEMA's Flood Map Service Center and zoom to your address. The Harris County Flood Control District also published a user-friendly version at harriscountyfemt.org that allows you to compare existing and proposed flood zone boundaries side by side.

What About the Harris County Flood Bond Projects?

The 2018 Harris County Flood Bond, passed by voters after Harvey, authorized over $2.5 billion for flood mitigation. Many of those projects are now complete or underway. In some areas, completed channel and detention improvements have already reduced flood risk meaningfully, and those improvements are reflected in parts of the new draft maps. This is actually good news for some inner loop buyers. Ask your agent and check with the Harris County Flood Control District to see whether specific projects affect a property you are considering.

What Are the Honest Tradeoffs of Buying in a Flood Zone in the Inner Loop?

Buying in a flood zone is not automatically a bad decision. Plenty of smart Houston buyers do it every year with clear eyes. Here is how to think through the tradeoffs honestly.

The Case for Buying in a Flood Zone

Properties in Zone AE often come with pricing that reflects the added risk. If you are comparing two comparable homes and one carries a $200,000 price advantage because of its flood zone designation, the math on flood insurance may still work in your favor. Especially in a supply-constrained inner loop market, flood zone properties can represent real value for buyers who do their homework.

Many inner loop flood zone homes have been elevated, retrofitted, or rebuilt with modern flood-resistant construction since Harvey. A home that sits above its BFE with a favorable elevation certificate is a fundamentally different risk proposition than a home at or below BFE in the same zone.

The Case for Caution

If a property has flooded multiple times, has a history of insurance claims, or sits below its BFE, that is a different conversation. Properties with repeated flood history carry resale risk, not just personal financial risk. Future buyers will ask the same questions you are asking now.

Also watch for listings that disclose no prior flooding but are surrounded by evidence that says otherwise. If the permit records from 2017 show a major repair project, or if neighbors confirm the street flooded knee-deep, that tells you something the disclosure form may not fully capture.

How to Make Buying in a Houston Flood Zone Work

Get the elevation certificate. Get a real insurance quote during the option period. Review the Seller's Disclosure Notice line by line. Check both the current FEMA map and the 2026 draft map. Ask about mitigation history. And work with an agent who knows which questions to ask before you fall in love with a house.

I work with buyers across the inner loop every week, and the clients who navigate flood risk best are the ones who slow down in the research phase. Houston is absolutely worth buying in. You just need to buy smart.

If you are searching for inner loop homes right now, browse current listings here or explore Houston neighborhood guides to start with the areas that fit your risk tolerance and lifestyle.

Wrapping Up

Houston flood zones are a real factor in any inner loop purchase, and the landscape shifted in February 2026 with the release of new draft FEMA maps. The good news is that buyers who ask the right questions are in a strong position. Check flood zone designations on both current and draft maps. Get an elevation certificate if the property is near a flood zone boundary. Pull a real insurance quote before you commit. Read the Seller's Disclosure Notice carefully and push back on incomplete answers.

Flood risk does not have to be a dealbreaker in the inner loop. It has to be a known quantity. There is a real difference between the two.

Raquel Refuerzo has worked with inner loop buyers through two flood map revisions, Hurricane Harvey, and years of post-Harvey rebuilding. If you have questions about a specific property or neighborhood, reach out directly. This is exactly the kind of conversation worth having before an offer goes out, not after.

Related Keywords: Houston flood zones, inner loop Houston flood risk, buying home Houston flood zone, FEMA flood map Houston 2026, Harris County flood map update 2026, Zone AE Houston, Zone X Houston, Houston flood insurance cost, NFIP Houston, flood zone inner loop Houston, Houston flood disclosure, Texas seller flood disclosure, elevation certificate Houston, Base Flood Elevation Houston, Houston flood map MAAPnext, Harvey flood risk Houston, Houston flood zone by neighborhood, Montrose flood risk, Heights flood zone, EaDo flood risk, Midtown Houston flooding, flood insurance Zone AE Houston, private flood insurance Houston, Harris County flood bond, buying in Houston flood zone