Pick the Right Mortgage Loan Before a Payment Picks Your Lifestyle

You fall in love with a house in Houston. The layout works. The location works. The price looks manageable.

Then your lender sends two payment scenarios. Same home. Same price. Different mortgage loan. The monthly payment shifts more than you expected.

That is where most buyers get stuck.

Choosing between an FHA loan and a Conventional Loan is not about which one sounds better. It is about which one protects your payment, strengthens your offer, and fits your long term strategy.

Let’s break this down in a way that helps you make a confident decision before you submit an offer.

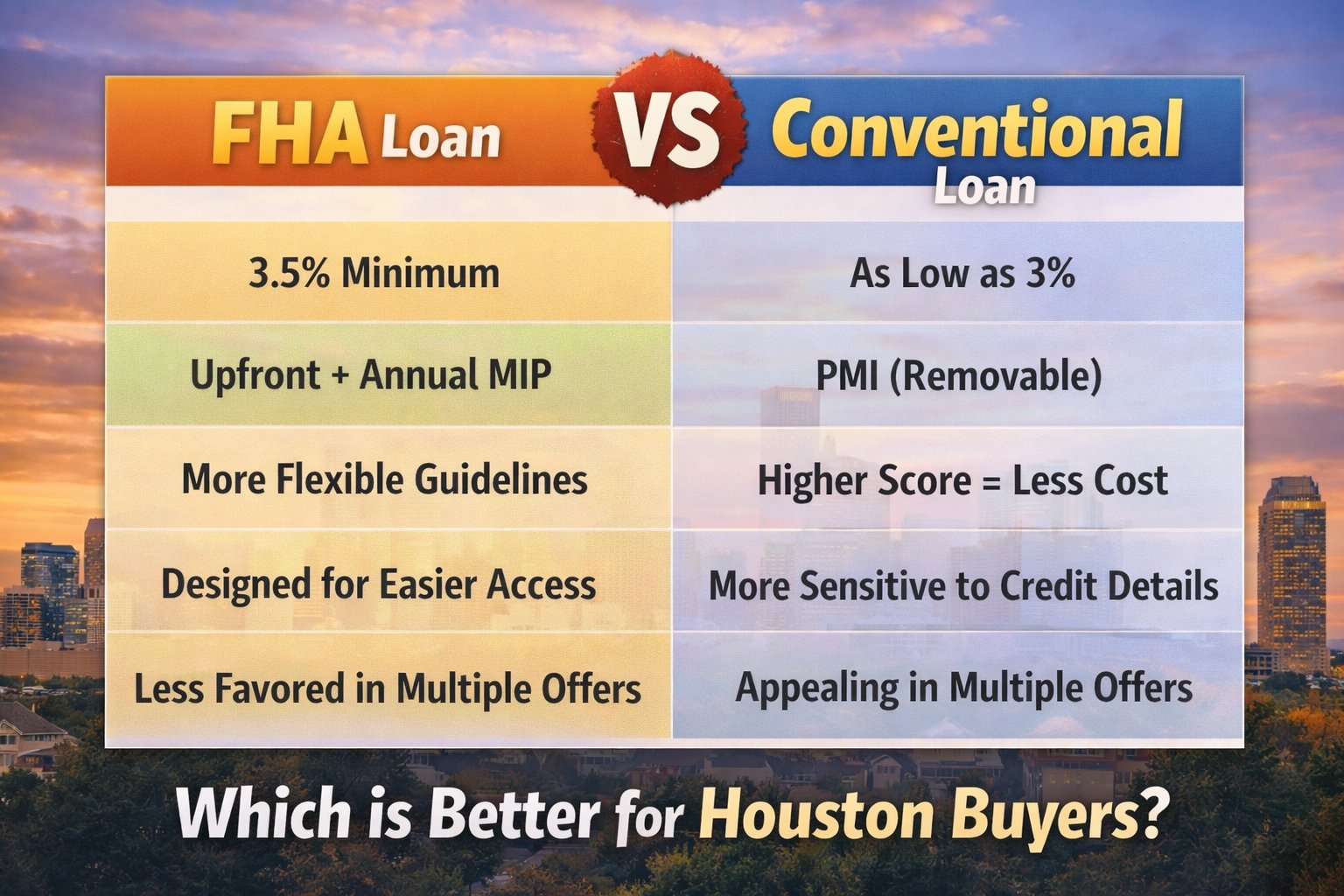

What Is an FHA Loan?

An FHA loan is a government insured mortgage loan backed by the Federal Housing Administration.

Key characteristics:

-

Minimum down payment often starts at 3.5 percent

-

Designed to help buyers with moderate savings

-

More flexible credit guidelines compared to many conventional programs

-

Includes mortgage insurance premiums

For many first time buyers in Houston, an FHA loan opens the door sooner than expected.

What Is a Conventional Loan?

A Conventional Loan is a mortgage that is not insured by a government agency.

Key characteristics:

-

Down payments as low as 3 percent in some programs

-

Private Mortgage Insurance, known as PMI, if under 20 percent down

-

PMI can often be removed once sufficient equity is reached

-

Strong appeal to sellers in competitive markets

For buyers with stronger credit profiles, conventional financing often offers more long term flexibility.

If you want a deeper overview of financing options, read:

Unlock the Secret Mortgage Hacks Every First-Time Buyer Should Know!

FHA Loan vs Conventional Loan: The Differences That Matter in Houston

1. Down Payment Requirements

Both programs offer low down payment options.

An FHA loan typically requires 3.5 percent down.

A Conventional Loan may allow as little as 3 percent down depending on qualifications.

If your priority is lowest cash to close, FHA often feels accessible.

If your priority is long term cost efficiency, conventional may outperform depending on your credit profile.

2. Mortgage Insurance Structure

This is where the real math lives.

FHA Loan

-

Upfront mortgage insurance premium

-

Ongoing annual mortgage insurance

-

Mortgage insurance may remain for the life of the loan in lower down payment scenarios

Conventional Loan

-

PMI required under 20 percent down

-

PMI often removable once you reach approximately 20 percent equity

-

Long term flexibility can reduce total cost

This distinction can significantly impact your monthly payment and total interest paid over time.

To understand how this affects affordability in Houston, read:

How Much House Can You Afford In 2026

3. Credit Score Sensitivity

FHA loan guidelines are often more forgiving with lower credit scores.

Conventional Loan pricing becomes more sensitive to credit bands. A 20 to 40 point difference in credit score can shift your rate and PMI cost.

If your score sits on the margin, FHA may provide more stability.

If your score is strong, conventional may reward you with better pricing.

4. Property Condition Standards

Houston has a wide mix of housing stock.

Older homes with deferred maintenance may face more scrutiny under FHA appraisal standards. Safety and habitability issues can trigger repair requirements.

Conventional loans often allow more flexibility depending on lender overlays and buyer risk tolerance.

If you are shopping in areas with older homes, this distinction matters.

A Real Houston Example

A recent buyer relocating to Houston was pre approved for both an FHA loan and a Conventional Loan.

Their target price was identical under both scenarios.

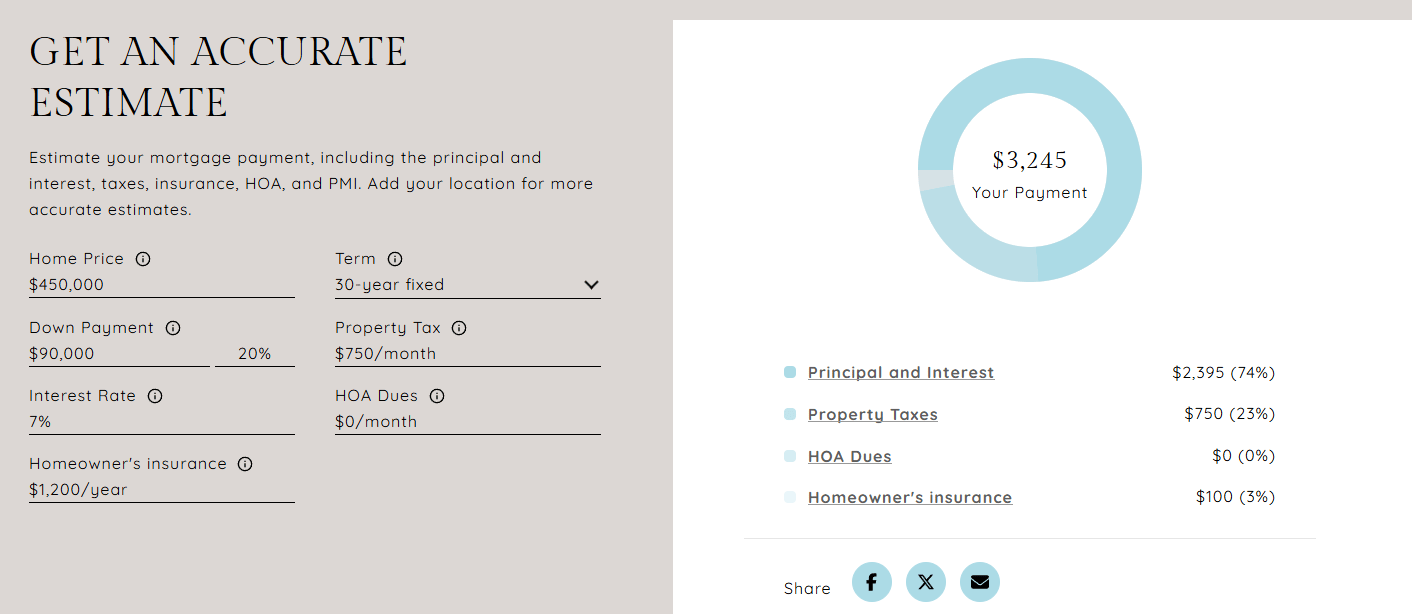

Once we ran the full payment including property taxes, insurance, HOA dues, and mortgage insurance, the difference became clear.

The FHA monthly payment ran higher due to the mortgage insurance structure. The conventional scenario carried PMI, but the long term cost projected lower because PMI had a clear removal path.

The buyer chose conventional and stayed in their preferred neighborhood without stretching their comfort zone.

The decision was not about approval. It was about payment structure and long term cost control.

If you want to avoid hidden costs, read:

The Hidden Fees That Could Derail Your Home Purchase And How to Avoid Them

When an FHA Loan Makes Sense in Houston

You prioritize access

You want a lower barrier to entry.

You have moderate savings

You prefer preserving reserves instead of maximizing down payment.

Your credit profile is improving

You plan to refinance into a conventional loan later when your equity and credit improve.

When a Conventional Loan Makes Sense in Houston

You want long term cost efficiency

PMI removal can reduce total cost over time.

You are entering a competitive neighborhood

Sellers often perceive conventional financing as lower risk.

You have strong credit

Better credit frequently translates into better pricing and lower PMI.

If you are preparing to compete in multiple offer situations, read:

Why Skipping This Step Could Cost You Your Dream Home

Decision Framework: Which Mortgage Loan Is Better for You?

Step 1: Define “Better”

Is better equal to:

-

Lowest monthly payment

-

Lowest upfront cash

-

Strongest offer position

-

Lowest lifetime cost

Choose one primary objective.

Step 2: Run Side by Side Loan Scenarios

Ask your lender for both an FHA loan and Conventional Loan estimate using:

-

Real Houston property tax rate

-

Insurance quote based on home age

-

HOA dues

-

Full mortgage insurance breakdown

Calculate your monthly mortgage in seconds with our free calculator HERE

Step 3: Stress Test the Payment

If rates shift before lock, does the payment remain comfortable?

If insurance increases at renewal, does the payment still work?

This is where confident buyers separate themselves from emotional buyers.

Frequently Asked Questions

Is FHA always cheaper monthly?

No. FHA allows lower down payment entry, but mortgage insurance structure may increase total cost over time.

Do I need 20 percent down for a Conventional Loan?

No. Many programs allow low down payment options with PMI.

Will sellers reject an FHA offer in Houston?

Not automatically. Strong pre approval, clean contract terms, and realistic repair expectations can make FHA competitive. Market conditions matter.

Where can I find down payment assistance?

Houston buyers should explore grant and assistance programs early.

Start here:

Are You Missing Out On Free Money?

Final Thought

The better mortgage loan is not the one your friend used. It is not the one your lender prefers. It is the one that aligns with your payment tolerance, equity plan, and offer strategy in Houston.

If you want a personalized breakdown of FHA loan vs Conventional Loan, connect with Raquel Refuerzo at www.RealtyRaquel.com

You will receive a side by side comparison tailored to your numbers, your neighborhood target, and your timeline.

Related Keywords: Houston mortgage loans, FHA loan requirements in Houston, Conventional Loan guidelines, FHA vs Conventional monthly payment comparison, PMI vs mortgage insurance premium, low down payment home loans, first time homebuyer Houston, Houston home loan credit score requirements, mortgage pre approval Houston, down payment assistance programs Houston, FHA appraisal requirements, Conventional Loan PMI removal rules, Houston property taxes and mortgage payment, and best mortgage loan for buying a home in Houston.