Buying your first home is a big step—and it can get confusing fast. Between different loan types, terms, rates, and fees, it’s easy to feel overwhelmed. But knowing the right mortgage strategies can actually save you thousands over the life of your loan.

As a professional Houston real estate agent, I work with first-time buyers every day and walk them through mortgage options that make the most sense for their goals. This article breaks down everything you need to know about mortgages—without the confusing lingo.

What Is a Mortgage and How Does It Work?

A mortgage is simply a loan used to buy a home. You borrow money from a lender, agree to repay it with interest, and the home serves as collateral.

There are a few main parts to a mortgage:

-

Principal – the amount you borrow

-

Interest – what you pay to borrow it

-

Escrow – a monthly account for property taxes and insurance

-

Amortization – how your loan gets paid off over time

You’ll usually choose between a 15-year and 30-year term. A fixed-rate mortgage keeps your rate the same, while an adjustable-rate mortgage (ARM) changes after a set period.

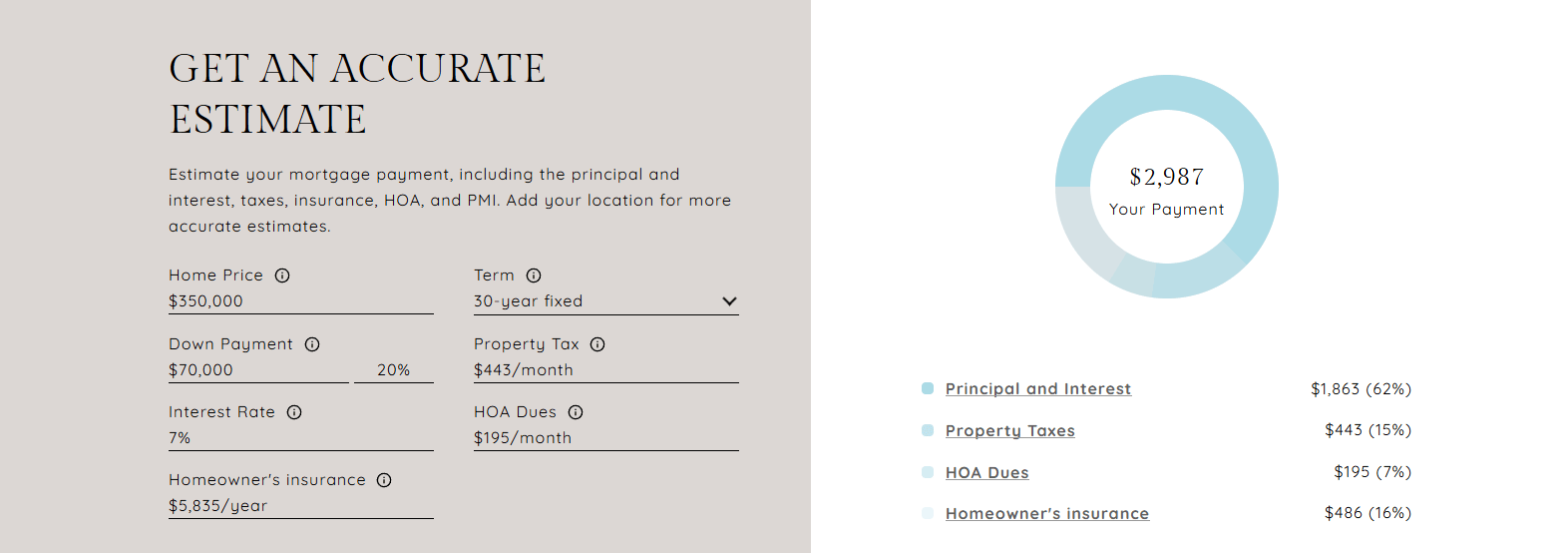

👉 Use our FREE Mortgage Calculator! Crunch the numbers, see your potential monthly payment, and make a smarter decision today! 🧮

Mortgage Types You Need to Know

Conventional Loans

These are backed by private lenders and not the government. You typically need:

-

A credit score of 620 or higher

-

A down payment (as low as 3%)

Pros: Better rates if you have good credit. Cons: Stricter approval.

FHA Loans

FHA loans are backed by the Federal Housing Administration and designed for lower credit scores and smaller down payments.

-

Credit scores as low as 580

-

Down payments starting at 3.5%

These are great for first-time buyers but require mortgage insurance.

VA & USDA Loans

If you’re a veteran or buying in a rural area, you may qualify for a VA or USDA loan.

-

VA loans: No down payment, no mortgage insurance.

-

USDA loans: Zero down payment in eligible rural zones.

Check eligibility on the USDA website.

Adjustable-Rate Mortgages (ARMs)

These offer lower initial interest rates for 5–10 years, then adjust based on the market. Best if you plan to move or refinance soon—but risky if you’re staying long-term.

Mortgage Hacks That Can Save You Money

Hack #1 – Shop Around (Seriously)

Every lender is different. A small rate change can mean big savings. Get at least 3 written quotes from different lenders and compare fees—not just the rate.

Hack #2 – Buy Down Your Rate

You can prepay interest by purchasing discount points, lowering your monthly payment.

-

1 point = 1% of the loan amount

-

Worth it if you’ll stay in the home for 5+ years

I’ve had clients save $50–$100/month by doing this upfront.

Hack #3 – Get Pre-Approved, Not Just Pre-Qualified

Pre-qualification is a guess. Pre-approval means your lender reviewed your documents and verified your finances. Sellers take your offer more seriously—and it speeds up closing.

Hack #4 – Take Advantage of Free Money

There are down payment assistance programs and first-time homebuyer grants that offer real money.

Are You Missing Out on Free Money? Top Home Buyer Grants Exposed (UPDATED)

Hack #5 – Watch Out for Hidden Fees

Loan estimates can sneak in extra costs:

-

Origination fees

-

Underwriting fees

-

PMI (Private Mortgage Insurance)

Always ask for a Loan Estimate (LE) and review it with your agent.

Credit Score Myths & Realities

You don’t need an 800 to buy a home. A 620–640 score is enough for many loans. But better credit = better rates.

Quick ways to boost your score:

-

Pay down credit cards

-

Avoid new credit inquiries

-

Don’t close old accounts

Myth: You need 20% down. Truth: Many buyers put down 3–5% and still get great loans.

Should You Work With a Mortgage Broker?

Mortgage brokers shop rates for you—but they also get paid through lender commissions. Ask them:

-

How many lenders do you work with?

-

What’s your fee structure?

-

Are there lender credits available?

If your credit is complex or you're self-employed, a broker may find better solutions than a bank.

Your Mortgage Timeline: What to Expect

-

Get pre-approved

-

Make an offer and go under contract

-

Submit documents to lender

-

Home appraisal and inspection

-

Underwriting review

-

Receive final approval (clear to close)

-

Sign documents and get the keys!

Keep communication open with your lender and agent to avoid delays. If something changes—like your job or credit—tell your lender immediately.

Real Talk From a Houston Real Estate Agent

I’ve helped dozens of buyers find homes and navigate financing—especially in markets like Greater Heights or Rice Military.

One of my clients almost settled for a high-interest loan because they didn’t shop around. After I recommended a local lender I trust, they saved over $14,000 in interest over five years.

These small decisions really add up. And you don’t have to figure them out alone.

Let’s Chat

Have questions about loans or buying your first home in Houston? Reach out—I’m Raquel Refuerzo, and I help first-time buyers navigate every step of the process, including financing.

Let’s make this less overwhelming (and even a little fun).

👉 Contact me today or explore my first-time homebuyer guide.

Related Keywords:

-

first-time homebuyer tips

-

Houston real estate agent

-

FHA loan vs conventional

-

how to get pre-approved for a mortgage

-

down payment assistance Houston

-

best mortgage hacks for first-time buyers

-

VA loan requirements

-

mortgage broker vs lender

-

closing costs explained

-

home loan timeline