It's March 2025, where the housing market is still defying logic and making us all reevaluate our budgets. Whether you’re shopping for your first home, upgrading, or downsizing, the truth is that what you think you can afford might not line up with reality. But don’t worry—I’m here to guide you through the chaos with real talk, practical advice, and a touch of sass.

What’s Driving Prices in 2025?

Let’s get one thing clear: The market isn’t expensive just to annoy you. It’s economics.

Interest Rates Are Still High

Mortgage rates are hovering around 7.5% for a 30-year fixed loan. Compare that to the 3% dream rates of a few years ago, and you’re paying a lot more in interest. A $400,000 loan now costs hundreds more per month than it did back in 2020.

Supply and Demand Imbalance

Houston, like many cities, still can’t keep up with demand. Builders are struggling with high material costs and labor shortages, and new homes aren’t popping up fast enough. Meanwhile, established neighborhoods close to downtown are holding onto their value because everyone wants in.

Inflation Hits Everything, Including Homes

Groceries, gas, and utilities are up—and so are property taxes and insurance premiums. That dreamy 3-bedroom, 2-bath home in The Heights? The taxes alone could rival your car payment.

Are You Champagne Tastes on a Beer Budget?

It’s time for a reality check. You might have fallen in love with a Pinterest-worthy house in River Oaks, but can you truly afford it?

Affordability Is More Than Your Mortgage

Say your lender pre-approves you for $450,000. That doesn’t mean you should buy at the top of your budget. You’ll also need to budget for:

- Property taxes (Texas doesn’t have a state income tax, but property taxes can sting).

- Homeowner’s insurance (especially for homes in flood-prone areas like Meyerland).

- Maintenance (that HVAC system won’t repair itself).

I had a client last year who insisted on buying a house with a pool. They didn’t realize the cost of upkeep would drain their budget (pun intended).

Use Online Tools Wisely

Affordability calculators are great, but they don’t account for real-world costs. Factor in utilities, HOA fees, and your lifestyle. Love dining out in Montrose every weekend? That’s got to fit in your budget too.

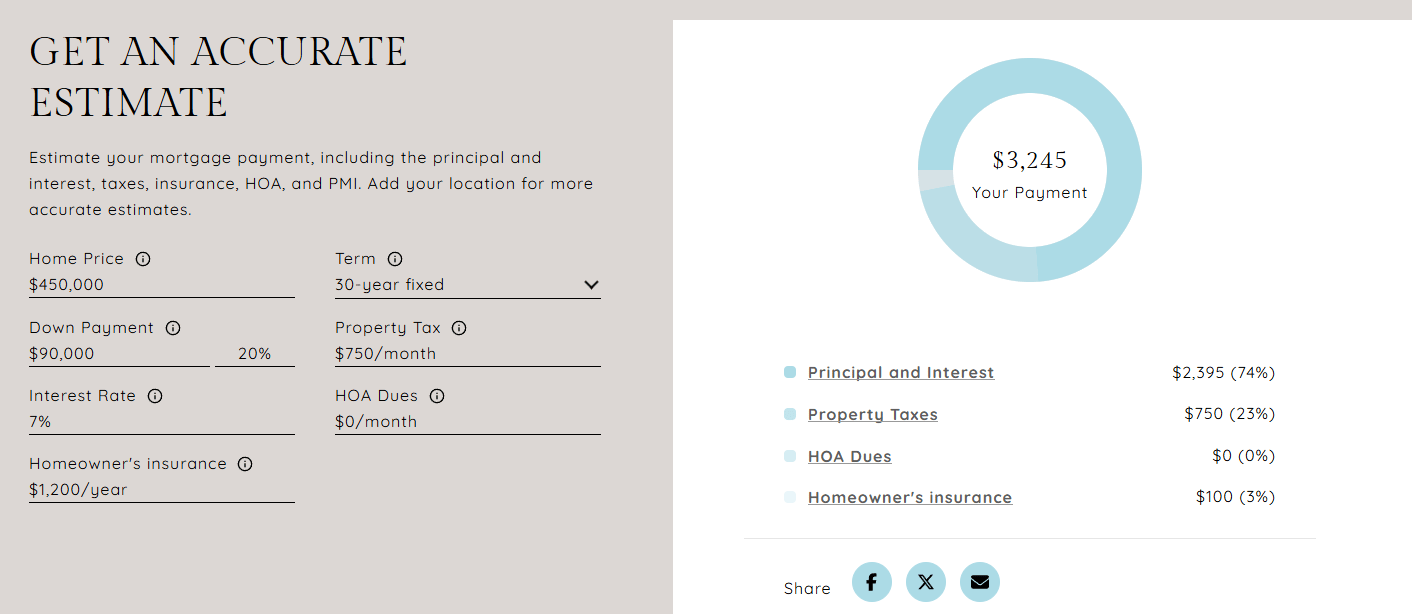

Realty Raquel | Free Mortgage Calculator

Location Matters More Than Ever

Where you buy affects what you get for your money. Houston offers plenty of options, but compromise is key.

Urban Convenience Comes at a Price

Neighborhoods like Midtown or the Museum District are walkable and close to everything, but you’ll pay for that convenience. Even a small townhouse could stretch your budget. Although, some may find that convenience of short work commutes and easy access to the best of what the city center has to offer totally worth it.

Suburbs Are the New Hotspots

Consider suburbs like Katy, Cypress, or Pearland. They offer more house for your money, plus good schools and growing amenities. Yes, the commute to downtown might add time to your day, but the trade-off is space and affordability.

Stretch Your Budget (Without Losing Your Mind)

You don’t need to max out your spending to get a great home.

Consider Alternatives

Look into FHA loans, which require lower down payments, or adjustable-rate mortgages (ARMs) if you plan to move within 5–7 years. They’re not for everyone, but they can save you money upfront.

Expand Your Search Radius

Widen your search beyond the city center. A 20-minute drive could save you tens of thousands. I’ve helped clients find amazing homes in Spring and Friendswood that they never considered.

Look for Hidden Gems

Fixer-uppers in established neighborhoods can be a smart move if you’re willing to put in the work. Think of them as long-term investments.

Red Flags You Can’t Afford to Ignore

Don’t let desperation push you into a bad decision. Be cautious about:

- Overpromising rental income: Buying a duplex in Houston with plans to rent out one side? Make sure demand supports your plan. Ask your agent for rental comps.

- Skipping inspections: Even in a hot market, never skip this step. A surprise foundation issue can cost tens of thousands.

- Taking on risky loans: An ultra-low down payment might sound appealing, but it could leave you underwater if the market shifts.

Let’s Find Your Realistic Dream Home

Ready to get serious about finding a home that fits your lifestyle and budget? As your local real estate pro, I’ll help you navigate the market with honesty, humor, and expertise. Reach out to Realty Raquel today—because you deserve more than just a house. You deserve a home you love (without losing sleep over the payments).